Your Child Wants to Study Abroad, Here's Everything You Need to Know

Aastha Sharma

Recently • 8 min read

It probably started with a casual conversation at the dinner table. Your son mentioned a university in Canada he'd been researching. Your daughter came home with a brochure about a program in Australia. And somewhere between the excitement in their eyes and the numbers you started quietly Googling at midnight, a familiar feeling settled in.

How on earth do we pay for this?

If that's where you are right now, this is written for you. Not the student doing the dreaming, you, the parent doing the math. Because funding a child's education abroad is one of the biggest financial decisions a family makes, and most of the information out there is either too vague to be useful or too optimistic to be honest.

Planning to Study Abroad?

Get personalized guidance from experienced education counselors.

If you're still evaluating whether abroad is even the right path, it may help to review the broader Study Abroad process before moving into funding decisions.

Let's fix that.

Start Here: What Does It Actually Cost?

Before you talk to a single bank or loan provider, you need a real number. Not a rough estimate. Not what someone's relative mentioned at a wedding. An actual, country-specific, program-specific cost breakdown.

Here's why this matters: the same university in the same country can cost dramatically different amounts depending on the program. An MBA at a Canadian university and a master's in computer science at the same university are not the same price. Tuition is just one piece. The full picture includes accommodation, food, health insurance (mandatory in most countries), books and materials, transport, visa fees, and flights home.

For most families looking at the UK or US, the total annual cost for a postgraduate student tuition plus living, ranges from 30 to 55 lakhs per year. Canada and Australia tend to be slightly more affordable than the UK, depending on the city. Germany is a genuine outlier public universities there charge little to no tuition even for international students, making it one of the cheapest countries to study abroad for Indian students when you factor in the full picture.

If your child is still comparing destinations based on affordability and career outcomes, reading How to Choose the Right Country to Study Abroad? can help align financial planning with long-term goals.

Get the real number first. The loan conversation comes after.

Understanding Education Loans, What Banks Actually Offer

Loan Category / Lender Type | Examples | Key Features | Loan Amount Range | Interest Rates | Processing & Flexibility | Best For |

|---|---|---|---|---|---|---|

Secured Education Loan | Offered by most banks | Requires collateral (property, fixed deposits, etc.) | Higher loan eligibility | Generally lower than unsecured loans | Standard bank documentation process | Families needing higher loan amounts at lower interest rates |

Unsecured Education Loan | Offered by banks & NBFCs | No collateral required | Usually capped at lower limits | Higher than secured loans | Faster approval in some cases | Students without collateral |

Public Sector Banks | SBI, Bank of Baroda, Union Bank | Dedicated study abroad loan products | ₹20 lakhs to ₹1.5 crore (e.g., SBI Global Ed-Vantage) | Lower compared to private lenders | Moderate processing time; collateral required above certain limits | Families prioritizing lower interest rates and longer repayment tenure |

Private Banks | HDFC Credila, Axis Bank, ICICI Bank | Faster processing, flexible documentation | Varies by profile | Higher than public banks | Quicker approvals | Families with urgent admission deadlines |

NBFCs / Specialist Education Lenders | Avanse, InCred, Auxilo | Education-focused underwriting; understand foreign admissions | Varies by lender and university profile | Typically higher than public banks | Flexible approach, especially for lesser-known universities | Students admitted to universities not immediately recognized by mainstream banks |

A few things worth knowing as you compare:

The moratorium period, the time between loan disbursement and when repayment starts, is typically the course duration plus six months to one year. This is when only simple interest accrues. The moment repayment kicks in, the EMIs on a large loan are significant. Have a clear-eyed conversation with your child about the job market in their field and country before signing.

Tax benefits exist. Under Section 80E of the Income Tax Act, the interest paid on education loans is deductible, with no upper limit on the interest amount and for up to eight years. This won't change the fundamental math, but it's a real benefit worth factoring in.

Before selecting a lender, compare documentation requirements, collateral expectations, and repayment structures carefully through the detailed Loan page, especially for secured loans.

Collateral, What Banks Want and What to Do if You Don't Have It

For loans above 7.5 lakhs (the threshold varies by bank), most lenders require collateral. This typically means residential or commercial property, or fixed deposits. For many families, this is straightforward, the family home is put up as security.

For families who don't own property or whose property valuation doesn't meet the loan requirement, the options are: co-applicants with stronger assets, unsecured loans from NBFCs (with higher interest rates), or, and this is important, aggressively pursuing scholarships to reduce the loan amount needed.

Which brings us to something too many parents skip in the funding conversation.

Don't Apply for a Loan Before Exploring These

The honest truth is that a significant number of Indian students who take large education loans could have reduced that burden substantially if they'd applied seriously for scholarships. Indian government scholarships for studying abroad are genuinely underutilised, not because they don't exist, but because families either don't know about them or assume they won't qualify.

The National Overseas Scholarship from the Ministry of Social Justice and Empowerment supports students from marginalised communities for postgraduate and doctoral study abroad, covering tuition, living allowance, and travel. If your family qualifies on income and category criteria, this can change the funding picture entirely.

The ICCR scholarships under cultural exchange agreements with various countries are another avenue, and again, under-applied for.

Beyond Indian government programs, country-level scholarships are substantial. Germany's DAAD program funds thousands of international students annually. The UK's Chevening is fully funded for postgraduate study. Australia Awards covers full costs for eligible students. And countries like Germany and Norway, which provide free or heavily subsidised education for international students at public universities, can make the loan requirement dramatically smaller even without a scholarship.

The combination strategy, partial scholarship plus a smaller loan plus part-time work income during the program, is how most families who navigate this well actually do it.

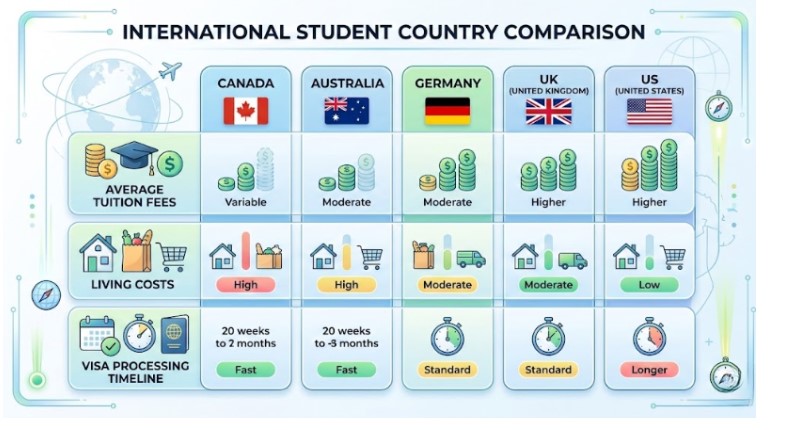

Canada, Australia, Germany, UK, US

A Quick Funding Reality Check by Country

Since these are the countries most Indian families are considering, here's the honest snapshot:

Country | Key Advantages | Tuition / Cost Overview | Living Cost Insight | Visa Processing Time | Loan Consideration Insight |

|---|---|---|---|---|---|

Canada | Strong post-study work opportunities, large Indian community, relatively clear immigration pathways | Tuition varies widely by university and program | High in cities like Toronto and Vancouver | 8–12 weeks (average) | Loan disbursement must align with visa approval and enrollment deadlines |

Australia | Excellent universities, structured post-study work visa system | Substantial overall cost | Expensive in Sydney & Melbourne; more manageable in Adelaide & Perth | 4–6 weeks (straightforward cases) | Graduates get time to build careers before aggressive loan repayment |

Germany | Minimal tuition at public universities, growing English-taught programs | Very low semester fees at public universities | Lower than London or Sydney; affordable in Berlin & Leipzig | Varies (generally moderate processing time) | Total loan requirement is often a fraction compared to other countries |

United Kingdom (UK) | Shorter master’s programs (typically 1 year) | High annual cost | High living expenses | Typically 3–6 weeks | One-year duration reduces total loan burden compared to 2-year programs |

United States (US) | Strong scholarship ecosystem, wide university options | Most expensive overall | High, depending on state and city | Varies widely | Merit scholarships available, but overall financial aid limited for international students |

If your child plans to stay back and work after graduation, ensure you understand post-study work rules and documentation timelines via the Visa page before calculating repayment schedules.

Questions to Ask Before You Sign Anything

Before you finalise a loan, from any lender, here are the questions that matter:

What is the exact interest rate, and is it fixed or floating? Floating rates sound attractive early but can increase significantly over a 10-15 year repayment period.

What happens if your child doesn't get a job immediately after graduating? What are the repayment flexibility options?

Is the interest simple or compound during the moratorium? This difference over two or three years of study is not trivial.

What is the total amount repayable if your child takes the full repayment tenure? Do that math before signing, not after.

Can the loan be prepaid without penalty? If your child does well and wants to close the loan early, this matters.

The Conversation Worth Having First

Before the bank visits and the loan applications and the collateral paperwork, have the honest conversation with your child about outcomes. What does the job market look like in their field in the country they're choosing? What salary can they realistically expect in the first two years? Can that salary support loan repayments while also supporting basic living costs?

This isn't pessimism. It's the responsible version of supporting your child's dream. The families who navigate education loans well are the ones who treated this as a financial plan, not just an admission decision.

If your family is still deciding whether studying abroad is strategically better than staying in India, reading Study Abroad vs Study in India – How Do You Actually Decide? can bring clarity before committing financially.

Your child's ambition is worth funding. Fund it smartly.

Start Your Study Abroad Journey

Join thousands of students who achieved their dreams with Yastudy.